Need the full summary? Open the long-form paper page.

Routing the Dollar

Gateway infrastructure, monetary policy transmission, and the dollar's international functions.

The problem

Dollar stablecoins now move hundreds of billions of dollars across blockchains, protocols, and regulatory jurisdictions. Whether this infrastructure strengthens or weakens the dollar's international functions depends on how it is governed. The conventional view treats each stablecoin as a product to be classified. This paper argues the policy-relevant unit is the gateway: the issuer, exchange, or protocol that routes the token. The same dollar token inherits distinct regulatory exposure, interest-rate sensitivity, and crisis behavior depending on which gateway processes it.

Three findings

Stablecoin supply moves with Fed policy, and the channel is dollar-specific.

Stablecoin supply is cointegrated with Fed balance-sheet variables in a pattern that strengthens when the Fed is tightening and weakens when it eases, even as the overall correlation remains strong. The relationship is absent for Bitcoin or Ethereum. A yield spread channel (the gap between Treasury bill rates and on-chain lending rates) provides mechanism-consistent evidence: when the spread widens, capital moves toward stablecoin reserves. Direct FOMC announcement effects are not significant, suggesting the channel operates through balance-sheet mechanics rather than forward guidance.

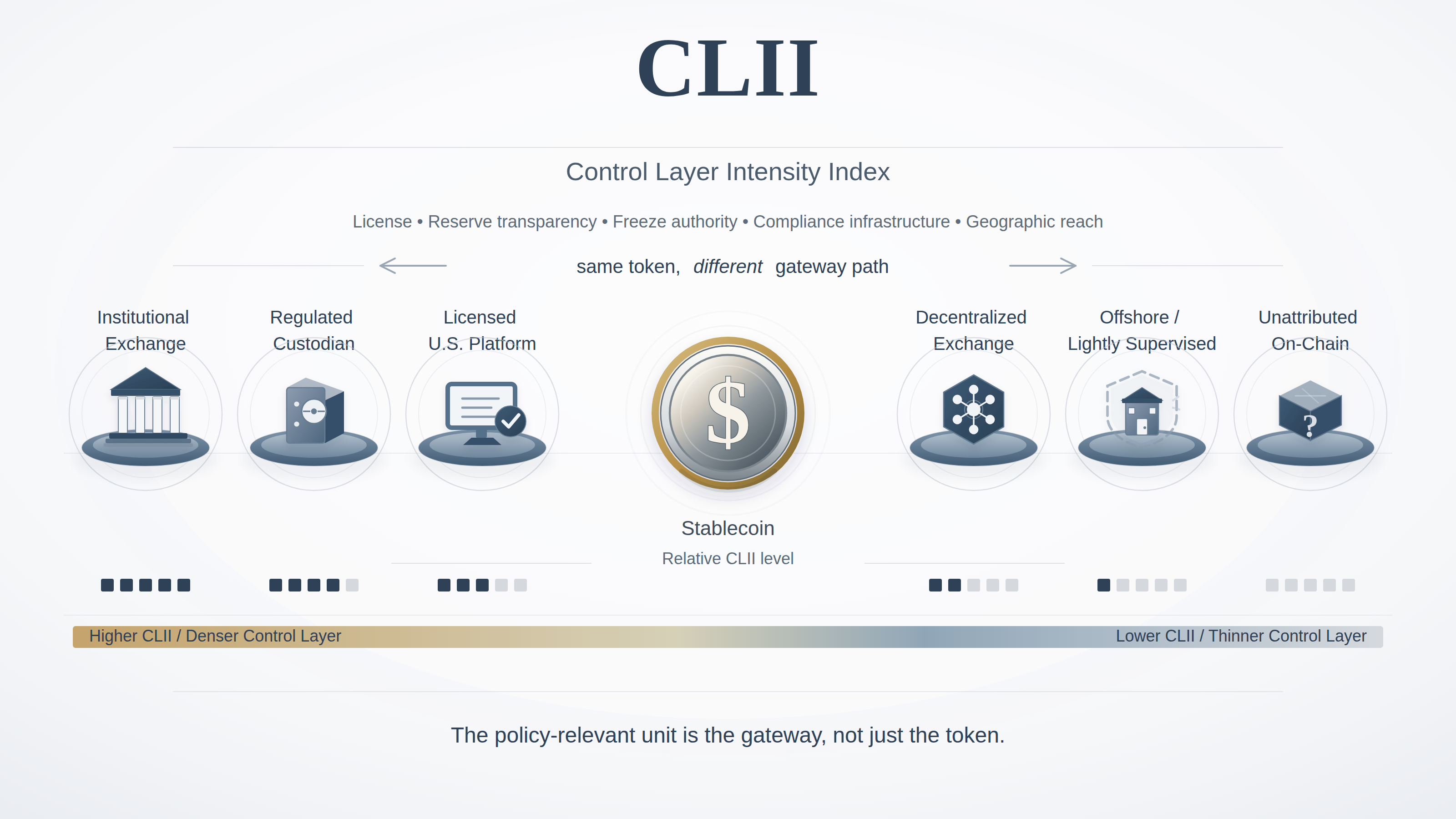

The same dollar token produces different regulatory outcomes depending on which gateway routes it.

The Control Layer Intensity Index (CLII) scores 19 gateway entities on five dimensions: licensing, reserve transparency, freeze capability, compliance infrastructure, and geographic restrictions. The routing network is concentrating: transfer volume doubled over three years while the number of distinct counterparties declined by a quarter and cross-gateway connections thinned sharply. Growth expanded usage; control consolidated.

During the SVB crisis, capital rotated across dollar gateways rather than exiting dollar instruments.

Regulated gateway share collapsed over a weekend as Circle's operations slowed, then recovered within days after banking-sector interventions. A permissionless smart contract temporarily became the primary dollar-routing mechanism. Three gateways with zero direct SVB exposure (MakerDAO, Paxos, Gemini) saw their instruments depeg through code-level reserve dependencies: contagion traveled through the gateway layer, not the token layer. Two gateways scoring within ten points of each other on the compliance index produced sharply divergent stress outcomes because their banking exposures differed.

Why it matters

Aggregate stablecoin supply is the wrong monitoring surface. Gateway-level flow data reveal the routing detail that aggregate numbers miss: which institutions are gaining share, which banking relationships create correlated exposure, and where settlement capacity fails under stress.

The CLII provides a five-dimension scoring framework for regulatory intensity at the gateway layer. It measures who is regulated, not who is fragile; two gateways with near-identical compliance scores can produce opposite stress outcomes depending on entity-specific exposures beneath the compliance surface.

The SVB evidence is consistent with a broader pattern: fragmentation in the digital-dollar system manifests as competition and concentration within the dollar's own gateway infrastructure, with limited substitution into non-dollar instruments. The strategic question for policymakers, issuers, and market participants is the same: who routes the dollar matters more than which dollar is routed.

Want to discuss this paper? [email protected]